I suppose many of us would have our own vision of retirement, and it’s eventually something which we would like to be able to do someday. It does seem to be increasingly difficult in Singapore as the years go by with the relentless increase in prices. People always find it incredulous when I say I’d like to retire soon – but that soon is probably a good 10 – 15 years away and it takes years of planning, saving and investing to eventually get there. My definition of retirement is being able to sustain a comfortable standard of living and being able to do what I like, whenever I like it. I don’t see myself needing much, spending my time on exercising, cooking and picking up some hobbies. I see myself volunteering, perhaps in animal shelters or working with less privilege children, maybe teaching and helping to set up schools in remote areas. I might set up a small online retail business, perhaps DIY some stuff and learn sewing. The husband and I have a private joke – that we will work in MacDonald’s together for some extra income and free food after retirement. Imagining us both old and in Macdonald’s uniform always puts a smile on my face.

Having said that, the current projection is to be financially free when we are around 45 – 50 years-old. It’s when our mortgage is fully paid and when our future children become almost fully independent. And of course, without kids in the picture, we can probably shave 10 years off the number. Perhaps it’s my financial background or perhaps it’s how my family has embedded the importance of money and savings since I was a child – I committed to my first regular savings plan when I was 21. It was an ILP which I have terminated this year, and I was lucky to make 1% p.a. despite the high fees throughout the 8 years. I was lucky to buy units very cheaply during the financial crisis that covered the hefty ILP fees. ILPs are definitely not the best way to grow your money, but without that, I wouldn’t have saved that 5-figure sum that was left untouched throughout the years. I also started a 15-year endowment plan when I was 25 for forced savings, and it matures when I’m 40. Many people started earlier, but many people have not started too. All too often, we hear complaints about how things are expensive and how retirement is but a dream – but these people need to understand that retirement requires years of planning and saving, sometimes making some sacrifices today for tomorrow’s freedom. What’s the point of complaining but not trying to find a way around it?

While I come from a middle-income family, my parents started out poor and have been thrifty all along. I started working at 15, during the June school holidays. A friend referred me for a job at Republic Plaza’s Coffee Bean. I worked for about a year there, part-time during school time. When my peers hung out at malls after school, I made coffee and cleared tables till late. It wasn’t that common around me, because most of my peers came from good families with ample pocket money to spend while my dad has always been very stingy with my pocket money. I hated asking for money, having to justify for why I needed it. I hated being dependent and not able to make my own decisions. I worked till I was 16, when I spent the last few months concentrating on my O’Levels. After O’Levels, I intended to take the Polytechnic route, and started working at DFS in the airport as a cashier at the Liquor and Tobacco shops. Money was pretty good and every single receipt keyed-in earned us an additional 5 cents in addition to our hourly pay. I ended up in Junior College, and worked every school holidays and sometimes during weekends for road shows selling things like Singtel/SPH subscriptions. I took up whatever odd jobs that the agency offered, mostly sales. I started teaching tuition after JC, throughout my university years. When I took up my first job upon graduation, my starting pay was lower than what I earned from part-time tuition during tertiary days. It was a big deal, because I charged barely $20/hr and my student base grew through word-of-mouth. Money was good, because they formed their own groups. Most of the days, I taught for 6 hours a day, back-to-back as they came to my place. Although I’ve wanted to stop teaching as it’s really tiring to teach 2 hours after work, I’m still teaching a few students now, for interest and some extra pocket money. Teaching has always given me the most satisfaction among all my ‘jobs’.

My parents would think that I’m a spendthrift, although I have always saved a large part of my income before spending. I’ve indeed spent a lot of what I earned on CDs and gadgets during my teenage years, and I’ve spent quite abit traveling around the world in the past few years. I guess there has to be a balance, in trying to save up but still being able to experience as many things as possible in life. Every penny spent on traveling has been worth it, as it has opened my eyes and changed me in incredible ways. The husband and I have also created many memorable travel experiences and developed together as a couple. We have always traveled quite frugally, never spending much on accommodation and food. I often wonder when can I travel Europe and enjoy their beautiful hotels and restaurants instead of backpacking and staying in hostels. We did have many unforgettable adventures with our backpacks though, and those memories are priceless. Now, we have also made the conscious decision to delay the purchase of a car and save as much as possible these few years before kids come along and expenditure rises. We can probably afford a car comfortably now, but that would also mean at least $12,000 a year lost in savings. I put aside more than half of my income nowadays, transferred to different accounts to prevent myself from seeing it and spending it. It makes me feel perpetually ‘poor’ and I sometimes delay my purchases till the next paycheck. This helps to rein in my expenditure.

Most people start their retirement planning too late and underestimate the power of compounding interest. What you choose to save instead of spend today will have far-reaching effects in the years to come. There’s also a big difference between saving up first before having children and having children first before saving up! People don’t get it why we want to delay having kids and see no difference in the expenditure now or two years down the road. I beg to differ!

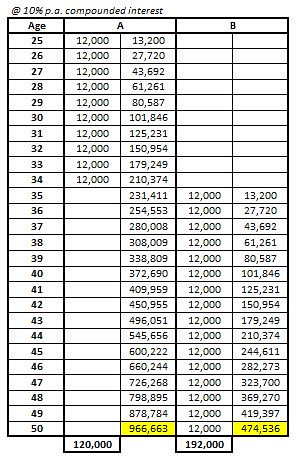

I have started my own portfolio of investments late last year, and would expect to make about 12% return this year through dividends and capital gains. To illustrate the power of compounding interest with a very simplistic illustration, assuming 10% p.a. compounded interest: If A were to save $12,000 a year for 10 years between ages 25 and 34, but stop saving after expenditure rises when kids come along, he will end up with $966,663 when he is 50. Compare that to B who starts saving $12,000 a year from age 35 till 50, he will have $474,536. Although B saved more than A, B has about half of what A has at age 50. Moreover, A doesn’t even save anything between ages 35 and 50! If the portfolio generates 6% dividends, a $1 million portfolio would have about $60,000 p.a. income, and that would be sufficient for a decent retirement lifestyle without even liquidating anything.

Of course, there are many variables throughout the years and cynics will have many reasons why this wouldn’t work. Some may even complain how difficult it is to even survive in Singapore, let alone save. Circumstances do change, but that doesn’t mean that plans should not be in place to react accordingly. As a matter of fact, it was worked for many regular working-class people, and some of them have shared their knowledge freely. For most, it’s not that difficult to save $1,000 a month when you have very little commitments in your twenties. It can be your bonus and AWS with a few hundred every month. Even if you save less, you will get there eventually with consistency throughout the years. Some may say that a 10% return is neither guaranteed nor achievable, but there are many books that one can read to improve their financial literacy to help you achieve that. Singapore shares represented by STI have generated a 8.8% total annual return for the past 10 years, not taking into account dividends. There are many Singapore companies which have given out a consistent dividend payout of around 5% the past many years. With a long time-horizon and taking advantage of market downturns, it really isn’t that difficult.

The good thing about such planning is that anyone can do it. You don’t need to come from a rich family or have a huge capital to start. It’s possible for any regular working adult who is willing to save a couple of hundreds a month, every month, for a good 10 years. It becomes increasingly difficult to have a good job beyond a certain age and our employment income faces an increasing risk as we age. You don’t want to be 50 and have to work till 60 or even 70 because you do not have enough to retire.

I do hope that Singaporeans would become more financially savvy and start planning their finances early in life. Investing is not the same as gambling. Singaporeans are very lucky to have no tax for capital gain and dividends received, and investing is a very good way to accumulate and preserve your wealth without letting inflation erode it. Hopefully, I will be able to impart my financial literacy to my future kids and help them have a head-start in life.

And maybe, someone might be inspired to start their own retirement planning. =)

No comments:

Post a Comment